When 'No Tax Increase' Depends on Which Math You Use

A campaign claim has been made that there were “No Tax Increases for 4 Years.”

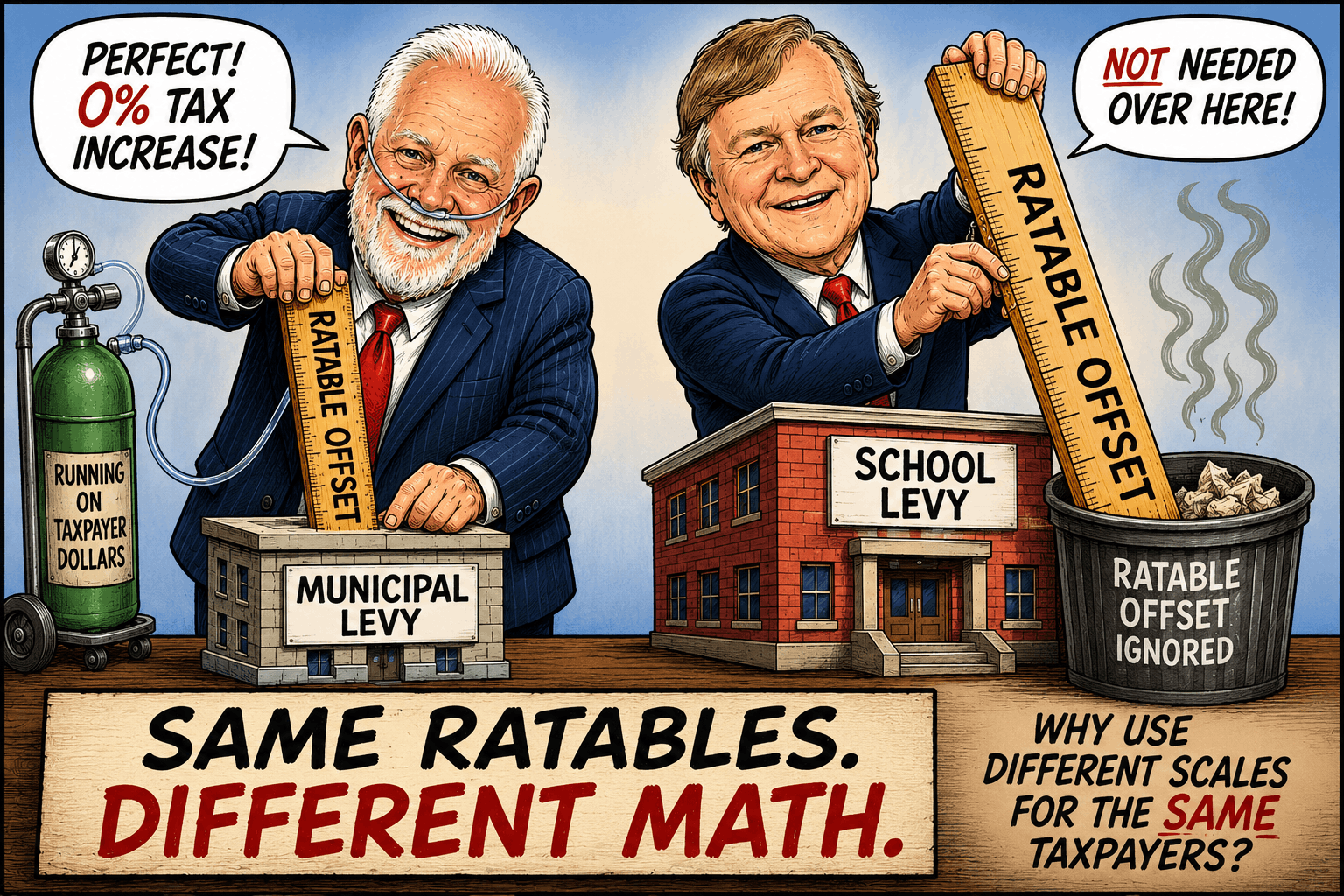

When challenged, the defense appears to be that new ratables helped offset the municipal tax increase.

That distinction matters.

There is a difference between saying:

“The municipal tax rate impact was offset by new ratables.”

and saying:

“There were no tax increases.”

Those are not the same statement.

Sourcing note: The dollar figures in this article are drawn from Hardyston Township’s 2026 municipal budget document, which reports the amounts to be raised by taxation for municipal, local school, regional high school, and county purposes, along with the township’s net valuation taxable. These are the township’s own published numbers, not estimates.

The Municipal Levy Still Increased

The township’s own 2026 budget document shows that the amount raised by taxation for municipal purposes increased.

For 2026, the municipal levy increased from $8,207,599.16 to $8,494,677.15.

That is an increase of $287,077.99.

At the same time, Hardyston’s net valuation taxable increased from $1,838,417,900 to $1,916,097,900.

That is an increase of $77,680,000 in ratables.

Because the tax base grew, those new ratables helped absorb the municipal levy increase. That may explain how someone tries to argue there was no impact on the municipal tax rate.

But that does not change the fact that the township still raised more municipal tax dollars.

Applying the Same Logic to the Schools

Here is where the argument becomes inconsistent.

If officials want to argue that the municipal increase was effectively “0%” because new ratables offset the increase, then the same logic should be applied to the school tax increases too.

The school levies also increased.

For 2026:

| Tax Levy | 2025 | 2026 | Increase |

|---|---|---|---|

| Local School | $11,861,878.86 | $12,325,393.76 | $463,514.90 |

| Regional High School | $7,260,270.24 | $7,705,196.19 | $444,925.95 |

| Combined Schools | $19,122,149.10 | $20,030,589.95 | $908,440.85 |

On the surface, that is:

| Tax Levy | Gross Increase |

|---|---|

| Local School | 3.91% |

| Regional High School | 6.13% |

| Combined Schools | 4.75% |

Why the Regional High School Rate Runs Higher

The regional high school number deserves a closer look, because it tends to surprise people.

Hardyston does not operate its own high school. It is one of several sending districts that share the cost of the regional high school district, and that shared cost — the regional tax levy — is not split evenly between the towns. It is apportioned by property valuation. Each sending district pays a share equal to its share of the region’s total assessed value.

Hardyston currently holds more than 52% of the property value in the region.

That means Hardyston pays more than 52% of every dollar the regional district raises — and more than 52% of every dollar of any increase the regional district approves.

So when the regional district announces a budget or levy increase, the percentage it advertises describes the district as a whole. It is not the percentage that lands on Hardyston taxpayers. Hardyston carries the largest piece of that increase, by design, because it carries the largest piece of the region’s value.

The share itself can also shift. If Hardyston’s property value grows faster than the other sending districts’, Hardyston’s slice of the region’s total value rises — and with it, Hardyston’s slice of the regional levy. When that happens, a modest districtwide increase can land as a steeper increase on the Hardyston tax line, because Hardyston is absorbing both the budget growth and a growing share of the total.

That is why the regional high school figure shown above is 6.13% rather than the smaller, districtwide number the regional district advertises. The advertised number describes the region. The 6.13% describes Hardyston’s portion of it.

The Ratable Offset

But if the argument is that new ratables offset the municipal increase, then the same ratable offset should be applied to the schools too.

Hardyston added $77,680,000 in net valuation taxable.

Using the combined school tax rate, those new ratables generated approximately $807,872 toward the school tax levies.

The combined school levy increase was $908,440.85.

That means approximately $100,569 of the school increase was not covered by new ratables.

If that remaining amount is split proportionally between the two school levies, the effective impact looks very different:

| Tax Levy | Gross Increase | Increase After Ratable Offset | Effective Increase |

|---|---|---|---|

| Local School | $463,514.90 | ~$51,290 | ~0.43% |

| Regional High School | $444,925.95 | ~$49,279 | ~0.68% |

| Combined Schools | $908,440.85 | ~$100,569 | ~0.53% |

So under the same logic used to claim a 0% municipal increase, the school increases are not 3.91% and 6.13% from a taxpayer-impact perspective.

They are closer to:

- 0.43% for the local K-8 school

- 0.68% for the regional high school

- 0.53% combined

You Cannot Use Two Different Standards

This is the issue.

If you measure the schools by the full levy increase, then the municipal budget must also be measured by the full levy increase.

If you measure the municipal budget after applying the ratable offset, then the schools must also be measured after applying the same ratable offset.

What is not fair is using one method for the municipal budget and another method for the schools.

That is how political talking points are created.

It is not how honest comparisons are made.

The Bottom Line

The township municipal levy increased.

The school levies increased.

New ratables helped offset the impact of both.

So the question is not whether taxes increased. The budget documents show that the levies increased.

The real question is whether it is honest to tell residents “No Tax Increases for 4 Years” while criticizing others using a completely different measurement.

If the claim is really:

“New ratables helped offset the municipal tax rate impact,”

then say that.

But that is not the same thing as saying there were no tax increases.